Overview

A synthetic dollar backed by real-world private credit and bonds.

Agama turns USDC into yield-bearing exposure to real-world lending — private credit and bonds — without a fund subscription, a lock-up negotiation, or picking a single deal blind. Deposit USDC, choose how directly you want to be exposed, and let the protocol do the allocation.

The problem

Private credit and bonds pay real yield, but that yield is locked behind slow, manual, fund-style access: subscription paperwork, minimum tickets, and settlement cycles measured in weeks. On-chain capital has no fast way in, and no way to diversify across deals without doing that paperwork many times over.

Agama wraps that access in two on-chain primitives: pick a pool directly, or mint a synthetic dollar that is automatically spread across every pool the protocol runs.

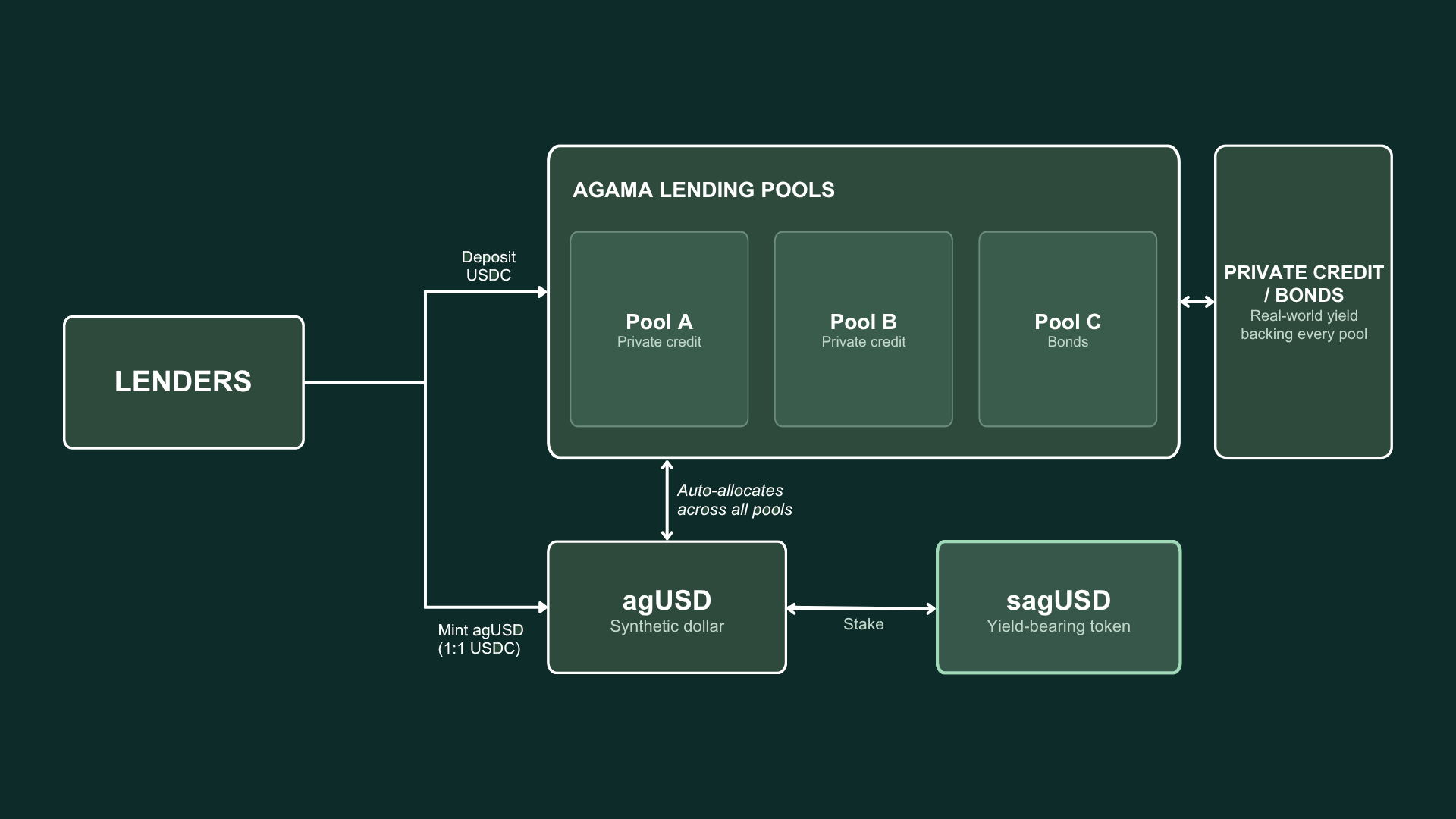

Architecture in one picture

Components

The protocol has three parts:

-

Lending Pools. Each pool funds one real-world credit or bond exposure — Pool A and Pool B are private credit, Pool C is bonds. Depositing USDC straight into a pool gives targeted exposure to that pool's real-world yield.

-

agUSD. A synthetic dollar, minted 1:1 against USDC. Instead of sitting in one pool, agUSD's backing is auto-allocated across every active Lending Pool — a single deposit that spreads across the whole book.

-

sagUSD. Stake agUSD to receive sagUSD, a yield-bearing token. Its value accrues over time as the underlying pools collect yield from private credit and bonds — no separate claim step required.

Two ways in

Agama deliberately supports both a direct and a diversified path, because they serve different users:

| Direct pool deposit | agUSD | |

|---|---|---|

| You choose | A specific pool (private credit or bonds) | Nothing — exposure is spread automatically |

| Exposure | Concentrated in one deal | Diversified across every active pool |

| Best for | Users with a view on a specific pool | Users who want blended, hands-off exposure |

| Upgrade path | — | Stake into sagUSD for yield-bearing exposure |

Where the yield comes from

Every pool's return is ultimately paid by real-world borrowers — private credit obligors or bond issuers — not by protocol emissions or other depositors. The Private Credit / Bonds layer in the diagram is that real-world backing: it's what every pool, and by extension agUSD and sagUSD, is earning against. See Lending Pools for how a pool is structured, and Risks for what can go wrong on the real-world side.

Getting started

- New users: read How It Works for a walk-through of both paths — direct pool deposits and minting agUSD.

- Depositors comparing pools: Lending Pools → Overview.

- Looking for yield-bearing exposure: agUSD and sagUSD.